Basement or Foundation Insurance Claims Step-by-Step

Dealing with basement flooding along with the attendant foundation repair can be stressful. Then there’s cleaning up and filing an insurance claim.

We have things covered when preparing to avoid basement flooding as well as repairing the foundation after flooding.

Here’s some insight into filing an insurance claim.

Safety First

Before you rush into the floodwater to begin your cleanup efforts, it’s absolutely critical that you move with caution. Safety must be first and foremost in your thoughts and actions.

- Turn off the electricity. Any water in your basement can easily find electrical outlets, wiring, appliances, and extension cords on the floor. That’s a sure recipe for electrocution. Turn off the main circuit breaker before going near the water. If that’s in the basement, call an electrician.

- Watch for natural gas leaks. If floodwater has caused the foundation walls to shift, their movement could easily crack or break pipes. A natural gas leak is an immediate explosion hazard. If you smell gas, leave the area and call the gas company.

- Stay clear of sewage backup. Another pipe at risk of cracking and breaking is the sewage drainpipe. Floodwater could cause it to back up. The resulting contaminated water in your basement is dangerous. Don’t enter it. Call a plumber.

- Beware of potential structural failure. That same movement of foundation walls could also lead to structural failure. That, in turn, could cause injury or death wherever you are in the house. If you suspect this level of instability, leave your home until it has been determined to be structurally sound.

As you can tell, there are some immediate dangers from basement flooding. Ensuring your safety and that of your family should be your first concern.

Step-by-Step Insurance Claims

Here are the key steps to file an insurance claim for basement flooding or foundation damage.

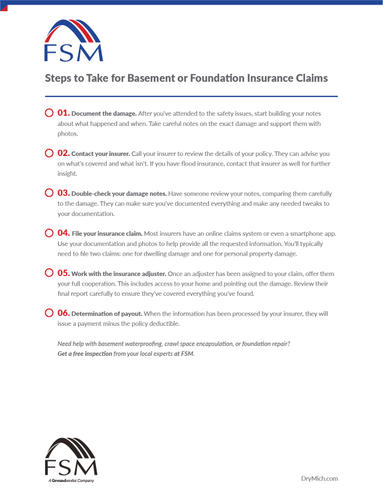

- Document the damage. After you’ve attended to the safety issues, start building your notes about what happened and when. Take careful notes on the exact damage and support them with photos.

- Contact your insurer. Call your insurer to review the details of your policy. They can advise you on what’s covered and what isn’t. If you have flood insurance, contact that insurer as well for further insight.

- Double-check your damage notes. Have someone review your notes, comparing them carefully to the damage. They can make sure you’ve documented everything and make any needed tweaks to your documentation.

- File your insurance claim. Most insurers have an online claims system or even a smartphone app. Use your documentation and photos to help provide all the requested information. You’ll typically need to file two claims: one for dwelling damage and one for personal property damage.

- Work with the insurance adjuster. Once an adjuster has been assigned to your claim, offer them your full cooperation. This includes access to your home and pointing out the damage. Review their final report carefully to ensure they’ve covered everything you’ve found.

- Determination of payout. When the information has been processed by your insurer, they will issue a payment minus the policy deductible.

For further information, FEMA has a helpful guide on How to File a Flood Insurance Claim.

Insurance Coverage: Basement Flooding and Foundation Damage

The typical homeowner’s insurance policy covers water damage from the overflow from sinks, baths, or toilets. It also includes burst pipes and leaking water heaters, dishwashers, or washing machines.

Basement flooding and foundation damage caused by weather events such as heavy rain, mudslides, sinkholes, or underground water seepage are not usually covered. For these hazards, you’ll need flood insurance.

Flood Insurance

Check with your insurance agent to see if supplemental flood coverage is available. You can also access FEMA’s National Flood Insurance program. They offer the FEMA Flood Map Service Center, where you can map your property to determine flooding risks and start the application process.

To add some perspective on flooding in our state, the First National Flood Risk Assessment estimated that 315,600 properties in Michigan are at substantial risk of flooding. In addition, the FEMA flood insurance program has seen 238,900 claims in our state since 2000.

FEMA has provided a cost of flooding calculator. Selecting a 2,500-square-foot one-story home and just one inch of water, the damage estimate is $26,807. Ramp that up to six inches and the expected damage reaches $52,037.

For more insight, see our article Top Cities in Michigan at Serious Risk of Flooding.

Basement Flooding Prevention

As always, it’s best to prevent flooding in the first place. To help your prevention efforts we’ve developed a Flood Damage Prevention Checklist. When you’re considering options for preventing basement flooding or foundation damage, it’s a good idea to get advice from professionals. For a free inspection, contact the expert team at FSM.

FAQs

Typically, standard homeowner’s insurance does not cover basement waterproofing or seepage, but separate flood insurance might cover some water damage.

Insurance coverage depends on the policy and the cause of the damage. While sudden and accidental damage may be covered, damage due to poor maintenance or wear and tear typically is not.

Typically, homeowners’ insurance does not cover water damage in the basement due to maintenance issues. Verify your policy details with your insurance provider.

Leah Leitow

Publish Date:

Last Modified Date:

Our Locations

32985 Schoolcraft Road

Livonia, MI 48150

5985 Clay Avenue SW

Grand Rapids, MI 49548

2817 Bond St.

Rochester Hills, MI 48309

5555 Airport Hwy

Toledo, OH 43615

3805 Elmers Industrial Drive

Traverse City, MI 49685